ODISEA: ¿Se vienE una devaluación después delas elecciones?

8 November, 2021

Patricio Navia: La justificación de la violencia explica la subida de Kast

12 November, 2021Grim outlook for loan growth, bank profits in 2022 as Argentines head to polls

Credit growth in Argentina’s financial system and bank profits will remain under pressure from high inflation even if voters deliver a rebuke to the ruling Peronist alliance and force a policy shift in congressional midterm elections on Nov. 14.

Financial investments, not traditional credit operations, will continue to drive banks’ net income in the next few quarters, according to industry experts, with banks’ net income suffering if prices continue their upward trend. Meanwhile, private credit contribution to GDP is at a decade-low of 12%, according to S&P Global Ratings estimates.

The elections for a third of the seats in Congress’ upper chamber and nearly half those in the lower house could signal a political turning point. The Juntos por el Cambio center-right coalition is expected to defeat the ruling Peronist alliance, Frente de Todos, led by President Alberto Fernández. The outcome could leave Fernández as a lame duck president for the remainder of his mandate.

Persistently high inflation and prolonged political uncertainty have pushed Argentine banks away from lending in recent years. Institutions have relied heavily on instruments, such as central bank notes, to generate revenue and drive profits. As much as 87.2% of banks’ income was generated from price gains on securities and valuation adjustments during 2020, central bank data shows.

“More inflation will result in a greater impact on banks’ balance sheets,” said Ivana Recalde, a banking analyst with S&P Global Ratings. “Banks are in standstill mode. They are extremely liquid [but] there is little they can do.”

Meanwhile, loan growth will likely remain under pressure. Surging prices will hinder a post-COVID-19 economic recovery in 2022, as well as eat away at banks’ financial revenue on securities, according to analysts.

“It is going be to really hard for the government to avoid price increases in 2022,” Marcos Buscaglia, an Argentine economist and a founder at Alberdi Partners, said in an interview. “The magnitude of the monetary expansion generates a peso overhang that stokes inflation down the road.”

Prices have soared 37% year-to-date, well above the government official estimate of 29% for the year.

“Independently of what the next Congress looks like, we are going to see a spike in inflation next year and a depreciation of the peso in real terms,” Buscaglia added.

Impact on banks’ balance sheets

Inflationary adjustments have been a major downward driver in banks’ balance sheets during the 12 months to August 2021, central bank data shows. Some 552.2 billion Argentine pesos, or nearly a third of banks’ financial margin, have been subtracted under so-called “monetary adjustments.”

“[Loan participation in GDP] is by far the lowest in the region,” Pablo Firvida, investor relations manager with Grupo Financiero Galicia SA, said in an interview. “And it is getting even lower compared to the last three or four years.”

Bankers argue that demand for credit has evaporated in the economy. Companies are not taking out loans and individuals are avoiding indebtedness in the current economic context. Higher inflation lifts nominal rates on loans to the point that they become unaffordable to most Argentines.

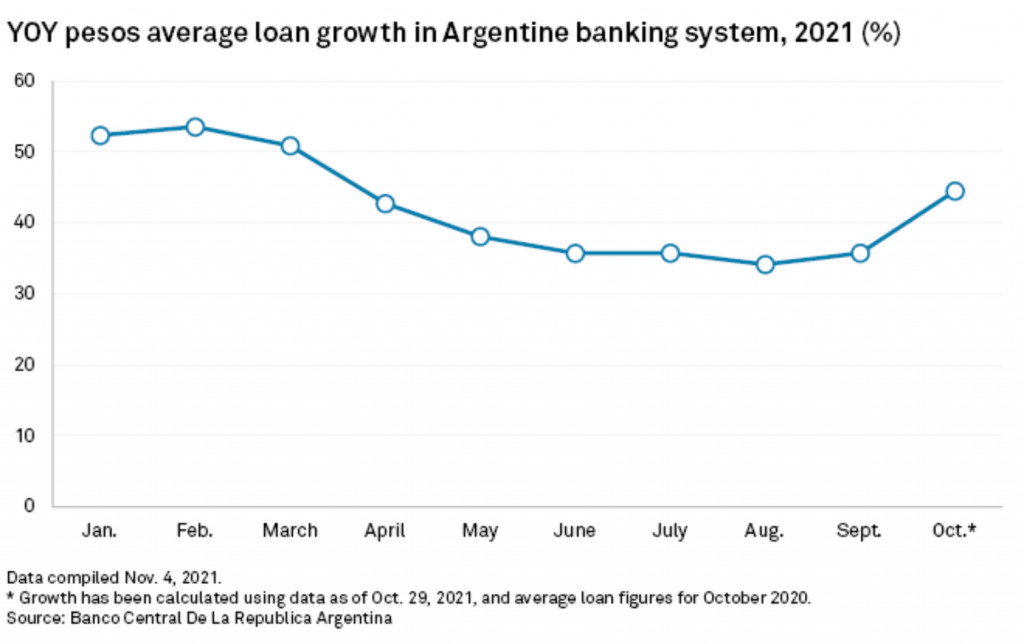

As subsidized credit lines from the COVID-19 pandemic lost steam, real loan book expansion took a downturn. Loans to the private sector in pesos reached a 39.25% year-over-year increase in October but were still negative in real terms due to inflation.

U.S. dollar-denominated loans, furthermore, have scaled back to five-year lows. Total loans in foreign currency hover above $4.7 billion, less than half of the $12.6 billion outstanding just two years ago. The return of a Peronist government has spurred a withdrawal of U.S. dollar deposits since 2019. In turn, banks have reduced their exposure to foreign-currency assets and stopped lending.

“We do offer [credit] products and want to grow but for that, we need demand to respond,” Galicia’s Firvida said. “That is simply not happening.”

While a quick look at year-over-year loan growth figures in pesos in Argentina’s financial system appears to show a fabulous performance, that nominal rise is actually a decrease in real terms when runaway inflation of more than 50% is factored into the equation. A more realistic picture of anemic credit growth is reflected in the loans in foreign currency, which have shown a steady decline over the past two years.

Profitability at major banks suffered, with return on equity dropping sharply in the second quarter of the year for most major banks in Argentina.

After the elections

Even in the likely event that Juntos por el Cambio emerges from the legislative elections with greater political clout in Congress, analysts are skeptical that the results will generate the momentum needed to change course and begin to normalize the distortions plaguing Argentina’s economy: increased levels of poverty, depreciation of the currency, unbridled inflation, foreign exchange restrictions and stagnant talks with the IMF over an estimated $44 billion debt.

Since its defeat in the August primaries, the Peronist alliance reshuffled its cabinet but doubled down on existing economic policy: it aggressively expanded its fiscal expenditure while at the same time imposed temporary price caps on more than 1,400 goods.

“Much of what happens the day after the election will depend on the magnitude of the [government’s expected] defeat,” Ignacio Labaqui, a senior analyst with Medley Global Advisors, said in an interview. He argues that for the government to tame inflation and currency pressures, a broad economic plan is needed, but that there are low chances of it coming to fruition.

“It would be reasonable for the Government to reach an agreement with the IMF and come up with some form of stabilization plan,” Labaqui said. “But that scenario is not likely, [and] I am not expecting a Copernican turn in economic policy.”

Once the election passes, there will still be a lot to be done. With spiraling inflation and a higher fiscal burden, the economic policy in Argentina remains unpredictable for the years to come.

“All in all, I am not expecting a good outlook for banks in 2022,” Alberdi’s Buscaglia said. “I am very optimistic about banks in Argentina over the long run. But in the short term, I think it is time for them to put the helmet on.”

As of Nov. 11, US$1 was equivalent to 100.18 Argentine pesos.

LINK NOTA: https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/grim-outlook-for-loan-growth-bank-profits-in-2022-as-argentines-head-to-polls-67328660

{kind=link}

{kind=link}

{kind=link}